Renovating Return On Investment

Have a look at these charts, which compare your return on renovating, based on the value of the home being sold.

posted by PondPine.com at 8:34 PM

2 comments

![]()

NEWS, ARTICLES, ANALYSIS, STATISTICS, OBSERVATIONS, FORECASTS, OPINIONS, COMMENTS AND DATA ON THE HOUSING MARKET IN OTTAWA (ONTARIO, CANADA).

posted by PondPine.com at 8:34 PM

2 comments

![]()

posted by PondPine.com at 1:57 PM

0 comments

![]()

posted by PondPine.com at 1:24 PM

0 comments

![]()

Haunted Halloween House

Haunted Halloween House

posted by PondPine.com at 2:00 AM

0 comments

![]()

The Ottawa Housing Market Blog would like to remind you to replace smoke alarm batteries when setting your clocks back one hour on Sunday, October 29, 2006.

The Ottawa Housing Market Blog would like to remind you to replace smoke alarm batteries when setting your clocks back one hour on Sunday, October 29, 2006.

posted by PondPine.com at 1:49 AM

0 comments

![]()

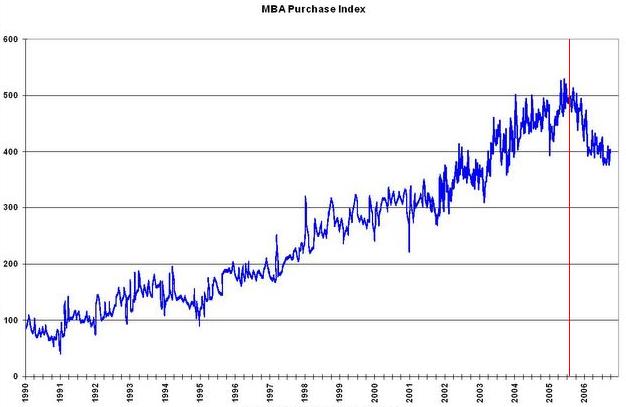

After the longest and most gravity-defying run-up in US house prices in history, the bubble has finally burst.

After the longest and most gravity-defying run-up in US house prices in history, the bubble has finally burst.

posted by PondPine.com at 8:36 PM

3 comments

![]()

posted by PondPine.com at 6:57 PM

0 comments

![]()

There have been rocky relations between the Bank of Canada (BoC), and the embattled Canada Mortgage and Housing Corp (CMHC).

There have been rocky relations between the Bank of Canada (BoC), and the embattled Canada Mortgage and Housing Corp (CMHC).I read with interest and dismay your press release of June 28 which indicated that CMHC would offer mortgage insurance for interest-only loans and for amortizations of up to 35 years.

Particularly disturbing to me is the rationale you gave that 'these innovative solutions will allow more Canadians to buy homes and to do so sooner'.

We were reassured by the fact that CMHC's interest-only mortgage product includes no change in mortgage qualification criteria and as such would not be of significant concern to the bank

posted by PondPine.com at 8:37 PM

0 comments

![]()

posted by PondPine.com at 4:32 PM

0 comments

![]()

posted by PondPine.com at 4:17 PM

1 comments

![]()

posted by PondPine.com at 7:30 PM

2 comments

![]()

posted by PondPine.com at 6:43 PM

0 comments

![]()

posted by PondPine.com at 6:35 PM

0 comments

![]()

posted by PondPine.com at 1:00 PM

0 comments

![]()

posted by PondPine.com at 7:16 PM

0 comments

![]()

The slowing housing market is forcing some real estate agents and builders to embrace unusual sales tactics.

The slowing housing market is forcing some real estate agents and builders to embrace unusual sales tactics.

posted by PondPine.com at 12:08 AM

0 comments

![]()

posted by PondPine.com at 11:27 PM

1 comments

![]()

posted by PondPine.com at 4:00 PM

1 comments

![]()

posted by PondPine.com at 2:10 PM

0 comments

![]()

Drop the Debt

Drop the Debt

posted by PondPine.com at 6:34 PM

0 comments

![]()

The U.S. economy continued to grow in the early fall despite a "widespread cooling" in the once-hot housing market.

The U.S. economy continued to grow in the early fall despite a "widespread cooling" in the once-hot housing market.

posted by PondPine.com at 4:00 PM

1 comments

![]()

posted by PondPine.com at 3:56 AM

0 comments

![]()

It is like the room of 1,000 Tim Hortons donuts. Even if they are warm donuts from Tim Hortons, how many can you eat? Three? Maybe four? And even if you come back the next day, and the donuts are now half price, how many can you eat? Same thing with housing. We only have so many people in the Canada. But builders built houses like donuts. They sold houses to non-users. They sold houses to the greedy masses that bought multiple houses to flip. Now we have the inventory, but there are not enough people to occupy these homes. Moreover, with interest rates rising and mortgages becoming tougher to obtain, we have less and less people that can buy these homes, even if they want to.

It is like the room of 1,000 Tim Hortons donuts. Even if they are warm donuts from Tim Hortons, how many can you eat? Three? Maybe four? And even if you come back the next day, and the donuts are now half price, how many can you eat? Same thing with housing. We only have so many people in the Canada. But builders built houses like donuts. They sold houses to non-users. They sold houses to the greedy masses that bought multiple houses to flip. Now we have the inventory, but there are not enough people to occupy these homes. Moreover, with interest rates rising and mortgages becoming tougher to obtain, we have less and less people that can buy these homes, even if they want to.

posted by PondPine.com at 3:37 AM

0 comments

![]()

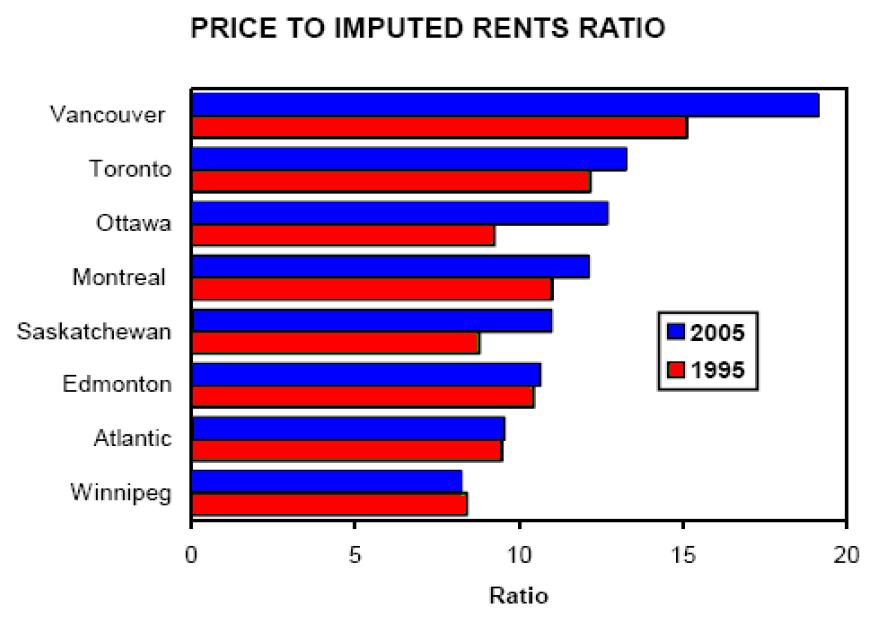

"Price to Rent ratio" or "Price to Earnings (P/E) Ratio"

"Price to Rent ratio" or "Price to Earnings (P/E) Ratio"

posted by PondPine.com at 3:11 AM

0 comments

![]()

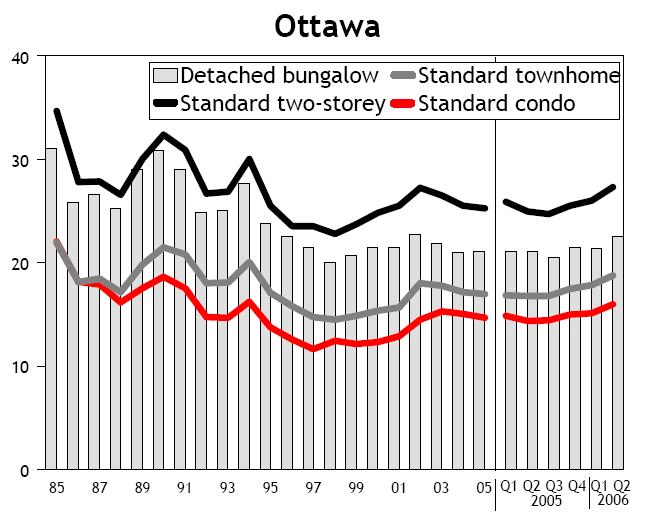

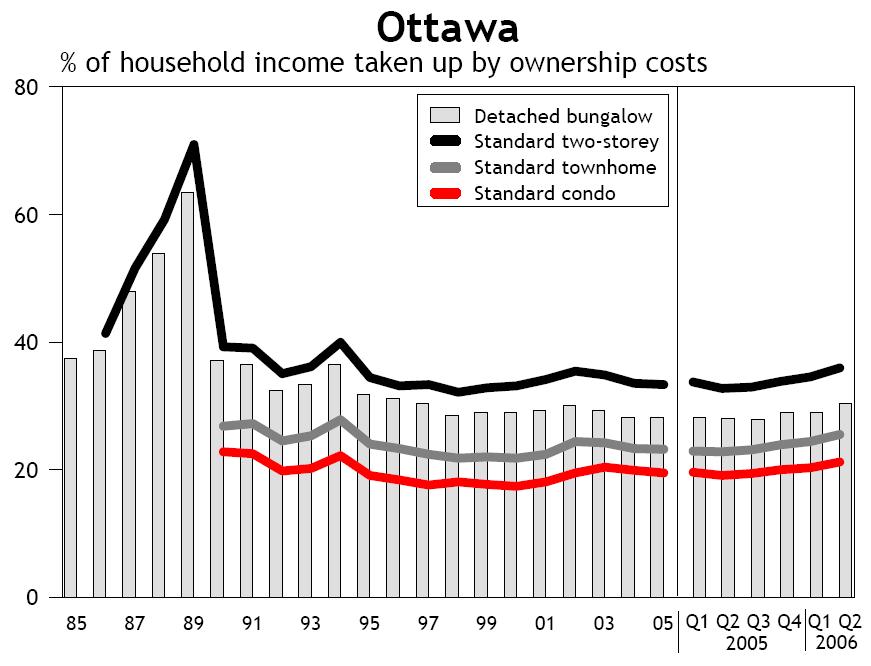

Ottawa standard housing affordability index measures the proportion of median pre-tax household income required to service the cost of a mortgage, including principal and interest, property taxes and utilities; the modified index used here includes the cost of servicing a mortgage, but excludes property taxes and utilities due to data constraints in the smaller CMAs. This measure is based on a 25% downpayment and a 25-year mortgage loan at a five-year fixed rate and is estimated on a quarterly basis. The higher the index, the more difficult it is to afford a house.

Ottawa standard housing affordability index measures the proportion of median pre-tax household income required to service the cost of a mortgage, including principal and interest, property taxes and utilities; the modified index used here includes the cost of servicing a mortgage, but excludes property taxes and utilities due to data constraints in the smaller CMAs. This measure is based on a 25% downpayment and a 25-year mortgage loan at a five-year fixed rate and is estimated on a quarterly basis. The higher the index, the more difficult it is to afford a house.

posted by PondPine.com at 2:44 AM

0 comments

![]()

Although housing affordability deteriorated across the board in the second quarter, conditions continue to remain fairly stable with little by way of affordability changes in the past decade. House price gains in Ottawa have been relatively more modest than in other markets in the past few years and have slowed to the 0-5% yearly range in every key housing class. Furthermore, the market is well-balanced between buyers and sellers with a sales-to-listings ratio of 0.6. Income growth has helped to offset the impact of rising mortgage rates, utilities costs and house prices. Except in the standard two-storey segment, qualifying incomes sit comfortably below average household income.

Although housing affordability deteriorated across the board in the second quarter, conditions continue to remain fairly stable with little by way of affordability changes in the past decade. House price gains in Ottawa have been relatively more modest than in other markets in the past few years and have slowed to the 0-5% yearly range in every key housing class. Furthermore, the market is well-balanced between buyers and sellers with a sales-to-listings ratio of 0.6. Income growth has helped to offset the impact of rising mortgage rates, utilities costs and house prices. Except in the standard two-storey segment, qualifying incomes sit comfortably below average household income.

posted by PondPine.com at 2:39 AM

0 comments

![]()

posted by PondPine.com at 4:27 PM

0 comments

![]()

The sizzling Ottawa housing market in Canada is prompting many residents to take out lines of credit, prompting a potentially inflationary burst in consumer spending.

The sizzling Ottawa housing market in Canada is prompting many residents to take out lines of credit, prompting a potentially inflationary burst in consumer spending.

posted by PondPine.com at 3:57 PM

0 comments

![]()

posted by PondPine.com at 2:54 PM

0 comments

![]()

posted by PondPine.com at 2:51 PM

0 comments

![]()

posted by PondPine.com at 2:46 PM

0 comments

![]()

The return on investment on a mid-range bath modernization is 102% of its cost. Kitchens can add about 90% of their costs to the home's value.

The return on investment on a mid-range bath modernization is 102% of its cost. Kitchens can add about 90% of their costs to the home's value.

posted by PondPine.com at 2:41 PM

0 comments

![]()

Ottawa Mayor announced his three point plan to beautify and boost economic development along St. Joseph Blvd. in the city's east end.

Ottawa Mayor announced his three point plan to beautify and boost economic development along St. Joseph Blvd. in the city's east end.

posted by PondPine.com at 3:24 AM

0 comments

![]()

Steadily rising home prices and the recent upward drift in mortgage rates is tilting the economics of housing back in favour of renting over home ownership.

Steadily rising home prices and the recent upward drift in mortgage rates is tilting the economics of housing back in favour of renting over home ownership.

posted by PondPine.com at 2:30 AM

0 comments

![]()

posted by PondPine.com at 1:59 AM

0 comments

![]()

posted by PondPine.com at 8:24 PM

1 comments

![]()

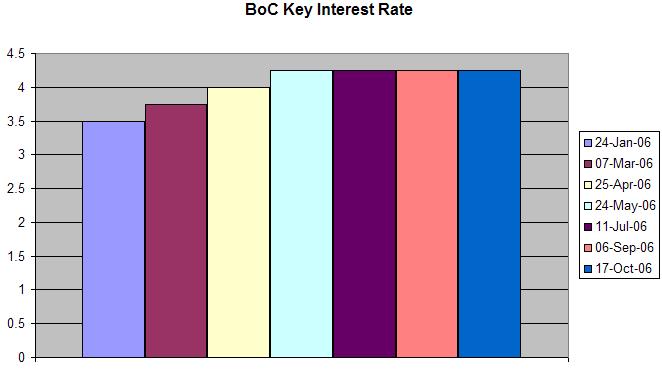

The Bank of Canada kept its benchmark interest rate unchanged for a 3rd meeting, cutting its growth forecast while saying the risks of high consumer spending and falling exports are "roughly balanced".

The Bank of Canada kept its benchmark interest rate unchanged for a 3rd meeting, cutting its growth forecast while saying the risks of high consumer spending and falling exports are "roughly balanced". The target rate for overnight loans between banks remains 4.25 %, the highest since August 2001 and 1 % point less than the Federal Reserve's target.

The target rate for overnight loans between banks remains 4.25 %, the highest since August 2001 and 1 % point less than the Federal Reserve's target.

posted by PondPine.com at 6:48 PM

0 comments

![]()

posted by PondPine.com at 6:39 PM

0 comments

![]()

posted by PondPine.com at 6:30 PM

1 comments

![]()

posted by PondPine.com at 5:07 PM

0 comments

![]()

posted by PondPine.com at 3:34 PM

0 comments

![]()

The federal government is quietly testing the waters about privatizing the national housing agency, Canada Mortgage and Housing Corp (CMHC). That could bring billions of dollars into Ottawa's coffers but would also upset social-housing advocates and possibly cause upheaval in the bond market.

The federal government is quietly testing the waters about privatizing the national housing agency, Canada Mortgage and Housing Corp (CMHC). That could bring billions of dollars into Ottawa's coffers but would also upset social-housing advocates and possibly cause upheaval in the bond market.

posted by PondPine.com at 5:55 AM

0 comments

![]()

The U.S. population is on track to hit 300,000,000 on Tuesday morning, and it's causing a stir among environmentalists.

The U.S. population is on track to hit 300,000,000 on Tuesday morning, and it's causing a stir among environmentalists.

posted by PondPine.com at 5:19 PM

0 comments

![]()

posted by PondPine.com at 9:22 PM

0 comments

![]()

The sharp weakening of the Ottawa property market is playing a major role in Ottawa's economic slowdown. The key movers are the falling housing construction and a significant rise in the mark-up rates, including those for the purpose of housing and construction. It is expected that the property prices will probably be flat or down for a while. The fall in prices in certain areas or former hot spots will be offset by stable showing in other previously unexplored parts of the Ottawa region.

The sharp weakening of the Ottawa property market is playing a major role in Ottawa's economic slowdown. The key movers are the falling housing construction and a significant rise in the mark-up rates, including those for the purpose of housing and construction. It is expected that the property prices will probably be flat or down for a while. The fall in prices in certain areas or former hot spots will be offset by stable showing in other previously unexplored parts of the Ottawa region.

posted by PondPine.com at 6:37 PM

0 comments

![]()

posted by PondPine.com at 1:56 PM

1 comments

![]()

Harper blamed the job losses on a "softening" of the American lumber market, where demand has dropped because rising mortgage rates have squeezed the housing market and reduced new home starts.Does Harper Understand How Housing Market Works ? No. He did not.

posted by PondPine.com at 7:27 PM

0 comments

![]()

I found this sponsored story in Ottawa Business Journal with billshit answers about the future of the Ottawa Housing Market from Ottawa Top Homebuilders as Minto, Urbandale and Tartan.

I found this sponsored story in Ottawa Business Journal with billshit answers about the future of the Ottawa Housing Market from Ottawa Top Homebuilders as Minto, Urbandale and Tartan.A reasonable market, strong first time homebuyers market, fair move-up market.Urbandale:

We have a relatively balanced market with a little more strength in the townhouse market than the single-family homes.Tartan:

We sell suburban housing in the south end and west end. The market has levelled off from a few years ago, but is still strong and stable, relative to the last 10 years or so.Q2: How has the market cycle of the past eight years impacted your business? What impact do you expect it to have going forward?

Minto has gone from building 500 homes a year to over 1,000 homes a year in that time period. Looking ahead, we are well positioned to respond to the market.Urbandale:

It's taught us to be more attuned to customer needs, in order to be able to react quickly to emerging trends. By offering a variety of home designs and lots sizes, in different locations, the company is better able to respond to changing market requirements in the future.Tartan:

Our business has grown over the pass six years, both in terms of the number sales and in the number of people working for us. If sales stay steady, we will continue with our current number of employees

posted by PondPine.com at 3:35 PM

0 comments

![]()

posted by PondPine.com at 3:21 PM

0 comments

![]()

posted by PondPine.com at 3:16 PM

0 comments

![]()

posted by PondPine.com at 3:09 PM

0 comments

![]()

posted by PondPine.com at 7:51 PM

0 comments

![]()

posted by PondPine.com at 11:13 AM

0 comments

![]()

posted by PondPine.com at 11:08 AM

0 comments

![]()

posted by PondPine.com at 5:59 PM

0 comments

![]()

Check this out: Scotiabank is offering no-money down mortgages.

Check this out: Scotiabank is offering no-money down mortgages.According to analysts, Scotia's entry into no-money-down mortgages gives it a unique product in the ultra-competitive mortgage market -- although the other banks could quickly follow its lead. For Genworth, this is a chance to seize market share on the insurance side, which for years was dominated by a single player: the government-owned Canada Mortgage and Housing Corporation.I don't think this is a huge deal. Downpayments have been very low anyway, and if a downturn hits the difference between a 5 or a 10% downpayment vs a 0% downpayment isn't huge.

posted by PondPine.com at 5:44 PM

0 comments

![]()

posted by PondPine.com at 5:35 PM

0 comments

![]()

posted by PondPine.com at 5:32 PM

0 comments

![]()

posted by PondPine.com at 5:27 PM

0 comments

![]()

posted by PondPine.com at 3:15 PM

0 comments

![]()

The value of building permits issued so far this year in Ottawa is down almost ten per cent from 2005 levels.

The value of building permits issued so far this year in Ottawa is down almost ten per cent from 2005 levels.

posted by PondPine.com at 3:07 PM

0 comments

![]()

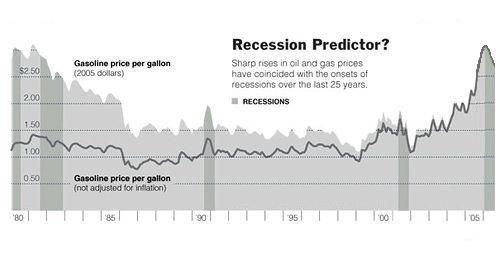

At the risk of sounding like a broken record, I have been cautioning since April that the surging commodity market, record high energy prices and overpriced housing were eerily reminiscent of the state of affairs that existed just before the high-tech bubble burst.

At the risk of sounding like a broken record, I have been cautioning since April that the surging commodity market, record high energy prices and overpriced housing were eerily reminiscent of the state of affairs that existed just before the high-tech bubble burst.

posted by PondPine.com at 2:52 PM

0 comments

![]()